If you want a thorough budget that will put every dollar to work for you, zero-sum budgeting might be the answer.

Think of your finances like a house. If the house is outdated or fallen into disrepair, you need a plan to remodel or rehab it. When it comes to your financial house, this plan would be your budget. Imagine that each room in the house represents a different goal such as growing your emergency savings, planning for retirement or paying off debt. Some areas of your financial house might need more work than others. For example, the bathroom you need to retile might represent your debt. Or the kitchen with that faulty sink in need of replacement might represent your savings.

Choosing a budgeting system is a lot like choosing the right approach to rehabbing or remodeling your home. You might spend months looking for the right contractor or figuring out how to do it yourself. The zero-sum budget, also known as the zero-based budget, can provide a holistic solution to revamping your finances.

Ashley Patrick, a financial coach and founder of personal finance blog Budgets Made Easy, is a dedicated zero-based budgeter and proof of how effective this approach can be.

“Since I started using the zero-based budgeting system, I paid off $45,000 in debt in just 17 months,” Patrick says. The zero-based budget system gave Patrick more control over her money, so she was able to make each dollar of income work harder for her.

How does a zero-based budget work if you, like Patrick, are trying to get more in control of your finances? Here’s everything you need to determine if this method is the best way to fortify your financial house:

What is zero-sum budgeting compared to other methods?

“Should I try a zero-based budget,” you ask? Zero-based budgeting holds a lot of appeal if you want to drill down into your finances and make every dollar work for your budget. Here’s how Nermeen Ghneim, owner of personal finance blog SavvyDollar, defines the budgeting method:

“The central concept of a zero-based budget is that you assign a dollar amount for each expense in a given month,” Ghneim says. Think of an expense as absolutely anything you put money toward, whether it’s bills, savings or investments. In the end, according to Ghneim, there should be zero unspent or unassigned money remaining in your monthly budget.

When addressing “what is zero-sum budgeting?”, it can be helpful to compare it with other types of budgeting. You may find that zero-sum budgeting provides a more purposeful, all-encompassing approach to managing your finances, with a strong emphasis on putting money aside for savings. For instance:

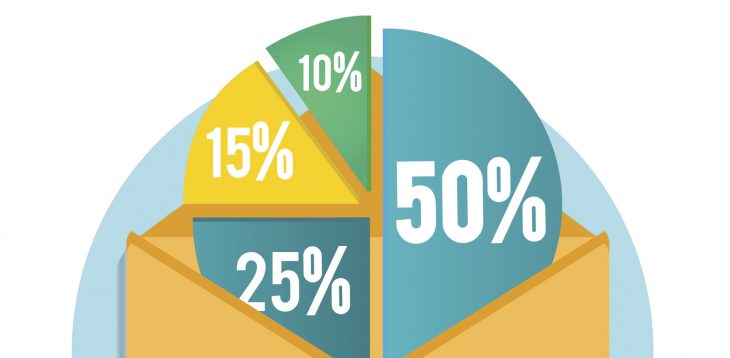

- The 50-20-30 rule directs 50 percent of your budget to living expenses, 20 percent to savings and investments and the remaining 30 percent to discretionary spending. If you are budgeting with the 50-20-30 rule, you would allocate all of your of savings (emergency fund, vacation fund, retirement investments, you name it) into 20 percent of your budget. On the other hand, with the zero-sum budget, you save whatever income is leftover after paying your essential expenses, and it motivates you to adjust this amount each month.

- With the half-payment budget method, you divide the cost of each regular monthly expense in half. If you’re paid bi-weekly, you set aside enough money to cover half of each expense following every paycheck. While this may be an effective method for paying necessary bills, it can fall short when it comes to bolstering your savings.

- Envelope budgeting means taking all of your expenses and assigning them to envelopes, then allocating cash to each envelope based on how much you plan to spend. The envelope budget is similar to zero-sum budgeting in that you’re assigning dollars to every expense category. With the envelope budget, however, you withdraw and use cash for everything.

Reasons why you should try a zero-based budget

At this point, you might be thinking, “should I try a zero-based budget?” The answer depends on how you’re currently approaching your budget and spending.

If you struggle with keeping track of your monthly expenses and haven’t tried any kind of budget before, the zero-sum approach could help you get some clarity on where your money is going—which, in turn, can help you be more purposeful with how you spend.

“Most people, if they even do a budget, just spend what’s left without thinking. But once you’re intentional with what’s left and make a plan for it, you’ll reach your financial goals much faster,” Patrick says.

The answer to “should I try a zero-based budget?” may be a resounding “yes” if you’ve tried other budgeting methods but they don’t seem to be working for you.

For example, if you’ve been using the 50-20-30 rule and you’re not saving as much as you’d like or you’re still fuzzy on what you’re spending, then zero-based budgeting could be a more effective concept to try. The same goes if you’ve tried the half-payment method but your income is too irregular to make that approach work.

Now that you know how a zero-based budget works, you may decide that it’s the right fit for your needs. The good news is that trying out the zero-based budget is easy.

How to start a zero-based budget in 5 steps

Time to give this a shot. Ghneim outlines five easy steps for trying a zero-based budget:

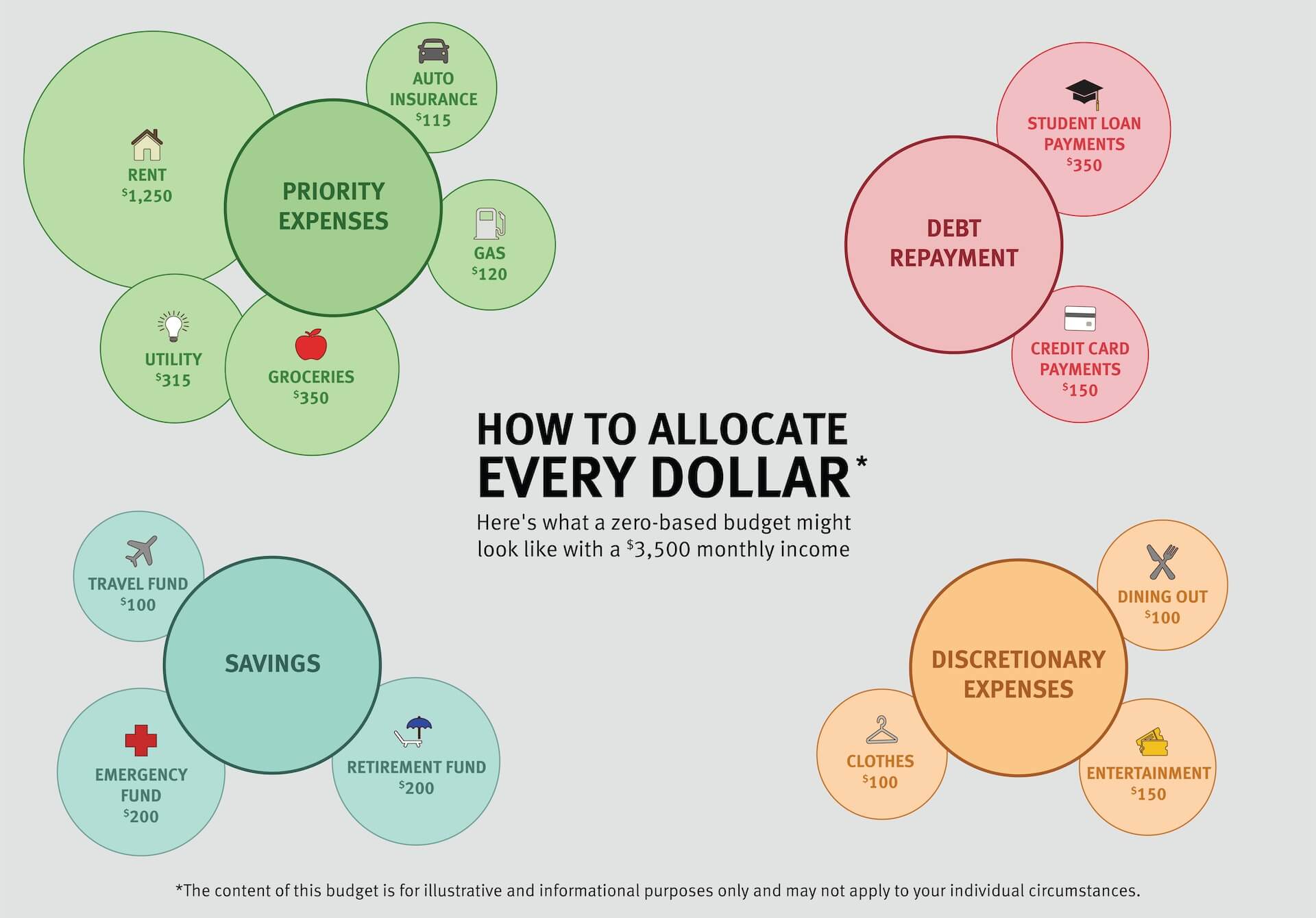

1. Determine your monthly income. How does a zero-based budget work? First, add up all of your household income for the month. If your paychecks aren’t always the same or you’re budgeting on a fluctuating income, you can use your average monthly income from the previous 12 months as a baseline for a zero-based budget.

2. Evaluate your expenses. Review your spending for at least two or three months, making note of your spending categories and your expenses within each. (Remember to divvy up quarterly or half-year bill payments equally over 12 months.) The easiest way to do this is to check your banking and credit card statements. Because some of your expenses vary from month to month, you’ll need to create a new budget before each month begins.

3. Assign priority expenses first. Take your total income and assign specific dollar amounts to each expense in your budget, starting with priority expenses like your mortgage or rent, utilities, food and transportation. You should be using the expense numbers you got in step two to do this. For example, if you know that your mortgage is always $1,000 a month, you’d automatically earmark $1,000 for that. If you average $600 per month on groceries, you can assign $600 to that category. Again, you’ll need to reassess these numbers each month when you create the following month’s budget.

4. Focus on debt repayment and savings. Once you’ve assigned money from your paychecks to your priority expenses, if you have money left over, continue working through your budget by assigning money toward your financial goals. “Once you have everything planned in your budget, put what’s left toward your goals, whether that’s saving or paying off debt,” Patrick says. Doing this can help you reach those goals faster, since you’ll be committing money to those budget items every month consistently. You may consider opening a Discover Online Savings Account to earn a competitive yield for your various savings goals.

5. Leave no dollar unassigned. The remaining money left is then assigned to your other expense categories, usually fun or discretionary, which includes dining out or entertainment.

At the end of this process, Ghneim says, every dollar of your income should be allocated to an expense or financial goal within your budget. Then, congratulations are in order. You’ve reached zero!

How to ensure your zero-based budget can work over time

Once you decide to try a zero-based budget, Ghneim says the two biggest challenges to keeping it going are: 1) taking the time to track your expenses each month; and 2) keeping an unexpected expense from wrecking your spending plan.

Once you get into the habit of following a zero-based budget, the tracking part could get easier, since your expenses may become more predictable each month. To keep yourself from going off-track, you might want to add an emergency fund category to your zero-based budget to cover any unexpected expenses that may arise. Financial experts suggest saving enough to cover three to six months’ worth of living expenses in an emergency fund.

Saving money can feel daunting, and you may struggle when you start determining how much you should put aside for the future. As you start learning how a zero-based budget works, tailor the amount you want to save to what’s realistic for you. For example, when you first implement this budgeting strategy, you might be able to commit only $50 a month to savings based on your current expenses or debt. But as you reassess your expenses each month and pay off debt or increase your income, for example, you might gain a little more leeway and be able to increase that to $200 or $500 a month.

But what if you go through your expenses, assigning dollar amounts, and there isn’t anything left over to save? How does a zero-based budget work then?

“If you come up short, trim back on some nonessential categories,” Ghneim says. She notes a few strategies that, when you put your mind to it, really aren’t that hard—no matter your budgeting style: Avoid eating out, cancel unused or unnecessary subscriptions and consider switching to a bank with no fees. For example, Discover Cashback Debit and Discover Online Savings Account have no account fees, such as monthly maintenance or minimum balance charges.1

Practice makes perfect when working toward a zero sum

While the goal is to get your monthly budget number down to zero, don’t worry if your income and expenses don’t balance out the first few times around. Even if you’ve decided you should try a zero-sum budget, it can take time to perfect. But once you put it into motion, you’ll probably find that no matter what your financial situation or your savings goals, you can tailor it to your needs and build in a flexibility that might not be possible with other budgeting methods.

Remember that financial house in need of repair? If you got to the end of this article, you’re on your way to a renovation you can live with.