Have you been spending lots of time at home? Creating a household budget can help you get a handle on where you’re spending—and where you can find ways to save.

Love it or hate it, many Americans are spending more time at home. The coronavirus pandemic not only accelerated the work-from-home trend to warp speed, but it also shuttered schools and summer camps, scratched travel plans and canceled brunch and dinner reservations across the country.

Jen Dawson, a certified financial planner and managing director in Chicago, found that the uncertainty and stay-at-home lifestyle created by the pandemic prompted her clients to look at their financial situations in a new light.

“I think it just gives opportunities for people and families to reflect,” Dawson says. “‘What do we want out of life? What do we want from our money?’ Those conversations are really valuable.”

As Dawson’s clients reflect on their goals, they (and many others) are also wondering, “How should I adjust my household budget if we’re spending more time at home?”

How to optimize your budget for the stay-at-home economy in 4 steps

Ellen Rogin, a former wealth advisor and now a speaker, author and entrepreneur, notes that people across the country were affected by the pandemic in very different ways. While many workers were able to keep their jobs as they transitioned to working from home, many were not.

“There are people who have lost their jobs and are being forced to make difficult decisions,” Rogin says. “And there are people who are still employed and earning the same income they did before, who have more options as they decide how they’re spending their money now.”

Even if you’ve been spared serious financial challenges, you should still consider updating or creating a household budget or spending plan. This will allow you to determine how to save more money in the stay-at-home economy.

Rogin and Dawson encourage you to use this opportunity to ensure you’re at least staying on track to meet your savings goals—and at best, shortening your savings timelines. It’s also a chance to make sure that your spending habits, which have likely changed as you’ve spent more time at home, are maximizing your happiness.

Below, we break down insights from Rogin and Dawson into four actionable steps you can take to save money in quarantine while living the best life possible. It all starts with taking an objective look at how your spending habits changed as you transitioned to a more domestic lifestyle.

Read on to see how to save more money in the stay-at-home economy by creating a new household budget:

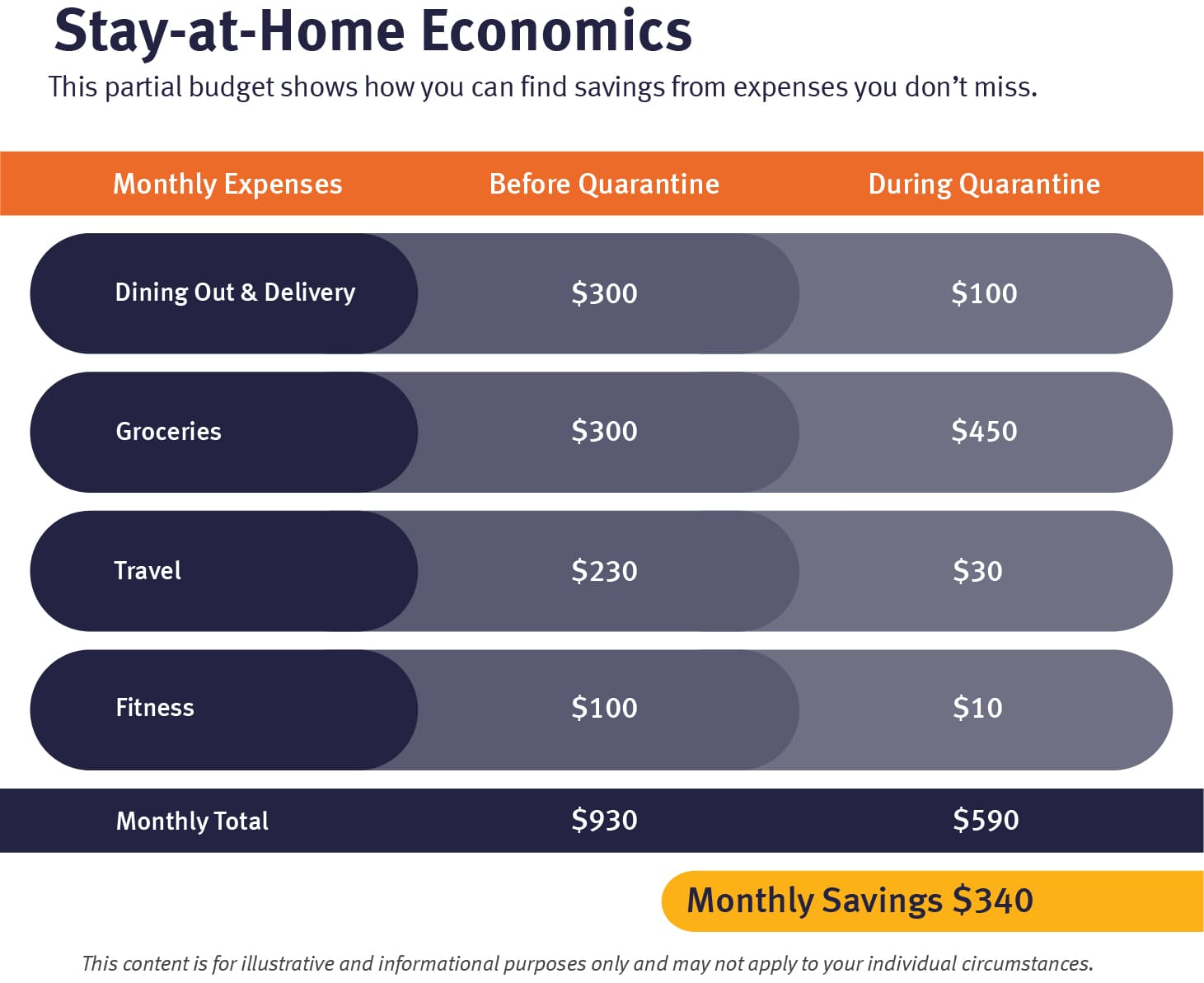

1. Compare your spending trends before and during quarantine

As you set about creating a household budget for an at-home lifestyle and determining how to save more money in the stay-at-home economy, start by reviewing your spending.

Dawson encourages you to refer to your debit and credit card statements to analyze the differences between your spending before staying home became the norm, and after. “You can compare it and contrast and have observations and discussions around what changed,” she says. “What do you like that you want to keep going, and what do you not like about it?”

All you need, Dawson says, is a spreadsheet to total up your major expenses, such as housing, utilities, transportation, food and dining, travel, shopping and entertainment. Then, subtract the sum of those costs from the money you earned (aka income) over the same timeframe.

Do this exercise for three months of spending before quarantine and then again for three months of spending during quarantine. You’ll be able to compare the data to see whether you have more or less disposable income as a member of the stay-at-home economy.

Rogin notes that it can be a little scary to examine your finances like this, but there’s no reason to feel anxious.

“Most people don’t really know how much money they’re spending, whether times are good or bad,” she says. “But it can really make you feel calmer to know what it takes to run your lifestyle.”

If you see that your disposable income decreased while in quarantine (or that you no longer have disposable income at all), then you’ll need to find ways to cut back on spending if you want to keep your savings goals on track. If your extra cash increased and you’re actually saving more money in quarantine, then you can start to consider how you might hit some or all of your savings goals more quickly.

Either way, you still have work to do as you consider how to save more money in the stay-at-home economy. Rather than focusing on external factors that are out of your control, Rogin and Dawson recommend that, as a next step, you ask yourself what matters most to you.

2. Ask yourself how your spending habits impact your happiness

Rogin considers the distanced, more remote way of life as a chance to reflect on what’s really important in order to create your household budget. One example she points to is how many people have been cooking at home far more often than they once did.

“Maybe you’re spending more on groceries, but that’s less than you were spending on eating out—and you enjoy it,” she says. “You’re spending more time with your family. You’re eating more healthily. So it gives you the opportunity to really assess your budget in a different way.”

Another example is travel. Rogin says that some people have told her that they really miss it, but others have been surprised to find how happy they are to pump the brakes on their jet-setting ways. In addition to saving money in quarantine from reimbursed travel and no more expensive trips, it’s allowed them to slow down and enjoy their time at home with family.

For her part, Rogin found that she wore the same two pairs of shoes during quarantine because they’re comfortable, and no one can see them when she’s video conferencing during work. As a result, Rogin cut this expense from her stay-at-home budget.

Whether you’re facing a cash shortage or surplus from more time spent at home, Rogin says that extending this line of thinking into a “values-based spending plan” for the stay-at-home economy will allow you to direct your money to what matters most to you, while diverting funds away from what doesn’t.

Once you add up the expenses that are no longer necessary in your stay-at-home budget, it’s time to put that money to work.

Tip: When looking at quarantine spending, don’t get too granular

Dawson underscores that evaluating spending patterns can be an emotional exercise. If you’re reviewing your finances with a family member, partner or spouse, try to resist the urge to nitpick every purchase. The trends should be easy enough to spot from a bird’s-eye view.

3. Put your stay-at-home savings toward your financial goals

Dawson and Rogin recommend having a plan when you’re trying to figure out how to save more money in the stay-at-home economy. That plan should include what you’re saving for, as well as where you’ll keep the funds as they add up.

Rogin recommends framing your financial goals from a positive angle. For example, when you create a household budget, instead of focusing on cutting spending, you can set a goal for how much extra money you want to save.

If you have children or live with a partner or spouse, Dawson notes that this goal-oriented approach can help get them involved. The objective might be to start an emergency fund to ride out unexpected headwinds. Or, the focus could be on saving up for a big vacation to look forward to when travel restrictions ease.

When deciding where to keep your savings, a standard checking account won’t allow your money to grow like a high-yield online savings account will. Rather than pooling the money you’ve saved in quarantine into one account, Dawson suggests opening multiple savings accounts, one for each of your savings goals.

“Be really clear about what each savings account is for,” she says. “Then you’re more likely to fund it.”

Of course, luxury savings goals like a vacation should not take priority over your long-term savings goals, such as retirement or college funds.

4. When saving money in quarantine, remember to support those in need if you can

If you are saving money in quarantine, Rogin suggests considering all the benefits of earmarking extra cash for philanthropic causes. It could go directly to the local small businesses you love that are hurting for revenue. Or it could go to any number of nonprofit organizations that are doing good in the world.

“So many people are in need now,” Rogin says. “There are so many beautiful ways that can help you feel like you’re making a difference for people by reallocating some of that money towards causes and people that you want to support.”

How will you start saving money in quarantine?

The stay-at home lifestyle may not have been in your plans, but you have the opportunity to gain control of your finances inside your home by creating a household budget that works for you in this new reality.

When you analyze, assess and optimize your spending and consider how to save money in quarantine, you’ll be in as strong a financial position as possible when life gets back to normal.

If you’ve been fortunate enough to save money in quarantine, consider starting or adding to your emergency fund. Not sure where to store your savings? Check out the four best places to keep your emergency fund.

Articles may contain information from third-parties. The inclusion of such information does not imply an affiliation with the bank or bank sponsorship, endorsement, or verification regarding the third-party or information.